You Need To Give Them Their Homes Back

U.S. Mortgage Crisis & Credit

Crunch

March 17. 2008

Sub Prime

Suspects:

|

|

|

Kerry "low budget Bill Gates" Killinger

|

Angelo "Tan Man" Mozilo |

Many costly

solutions to the massive U.S. mortgage crisis have been bantered

about, several undertaken with no success. There are now ghost

towns in pockets of the United States, as a result of millions

having lost their homes. Contrary to President Bush's

ignorant, irresponsible spin on the story in attempts at absolving his poor

presidency of any guilt in what transpired, it is not due to Americans buying

homes they couldn't afford.

The nerve of you. It's really rich coming from

someone whose granddaddy was banker to the Nazis. I see where you get your

banking policies from (Prescott Bush's Nazi affiliated "Union Banking

Corporation"). The Bush administration left the

banks unregulated and they went hog wild gouging the American people, producing

this unprecedented crisis.

Side Bar: the Bush family was also

involved in the Savings & Loan banking crisis of the 1980's that turned into a

big scandal.

S&L Times Twenty

(Neil, George jr., George sr. and Jeb Bush)

The current mortgage crisis makes the Savings And Loan crisis

of the 1980's look tame. The Bush family was mixed up in that one

as well, via Neil Bush running a failed bank the taxpayers had to bail out for

almost 2 BILLION DOLLARS and Jeb Bush defaulted on a loan that cost the

taxpayers $4,000,000.

The Savings and Loan crisis cost

the

U.S. taxpayer

$124.6 billion. The current banking crisis has cost the US

taxpayer far more. The Fed has already dumped several hundred BILLION into the

banking sector

in attempts at correcting the crisis. None of it has worked.

Savings and Loan story links:

Link 1 |

CONGRESSIONAL INTERVENTION

It was reported last week that the

government via Congress wants to buy up foreclosed homes, which I think is

unwise. That's just more spending on an already buckling treasury. You need to give people their homes

back that were foreclosed upon through fraud and or gouging. It would take

months, but it can be done. It is the correct, viable solution,

as opposed to wasting many billions in taxpayer money buying back homes that

went into foreclosure, because you failed to do your jobs in properly regulating

the banks the first time around.

Remove all the excessive fees and

financial penalties that were piled on these mortgages, put people back in their

homes where they left off before it went haywire, and at a decent, FIXED

interest rate, so they can make payments again on what they worked hard for

before it was improperly taken through gouging and fraud. It's better than blowing billions,

possibly trillions in taxpayer money to buy back homes you may not be able to

fill, as you destroyed millions of people's credit when you took their homes

through gouging and fraudulent foreclosure.

At this point there are probably

more people in America with bad credit than good. You do realize that? That's

another thing, you need to regulate credit card interest fees. Is there any

wonder people are always in debt when you have credit card companies charging

27% and 37 % interest.

Putting people back in their homes

is also better than the banks owning many and I mean many, vacant homes across

America that aren't selling at auctions, forcing them to do maintenance on the

properties and pay taxes on them as well. Then again, some banks like Washington

Mutual are idiotic and just might prefer that, as they are proud and very

corrupt.

However, to rational, logical

people, it is better to have occupied houses with money coming in as revenue,

than empty ones costing you money every month in taxes, lawn and other

maintenance fees.

It is better to have $1,000 per

month, $12,000 per year coming in, rather than an empty house. You multiply that

by the many foreclosed homes that ended up vacant due to gouging and fraud on

the part of the banks and that's substantial revenue for the lending

institutions, that would help them get back on track.

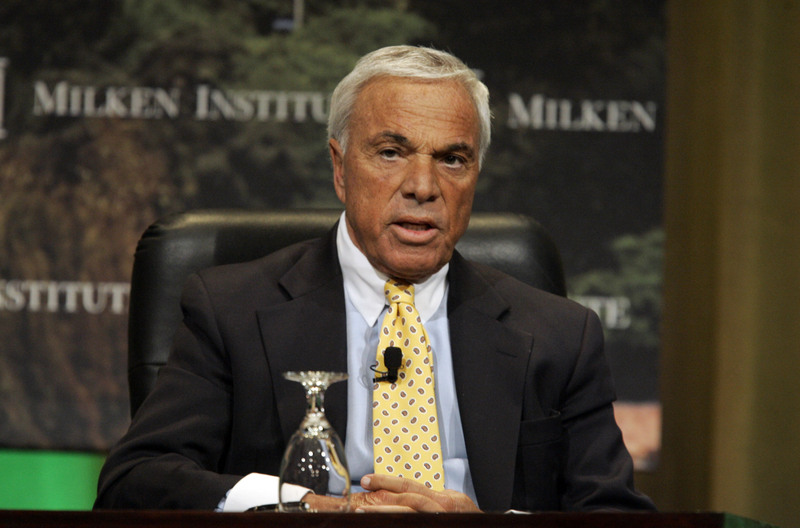

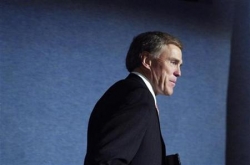

GOUGING RECAP

Angelo

Mozilo testifying in Congress this month

While millions of Americans

lost their homes via gouging and his company Countrywide began buckling, Angelo

Mozilo

walked away with a $168 million dollar golden parachute for his

terrible efforts and poor practices. As I wrote in my

December 13, 2007 article, "The CEO

leaves the company with a golden parachute when they should leave with a golden

indictment."

Several banks engaged in gouging

practices pioneered by Kerry Killinger at Washington Mutual and

Angelo Mozilo of Countrywide. The heartlessness under which they operate is astonishing.

Washington Mutual

They both became famous in the

banking world via offering cheapness that customers couldn't refuse. They

employed heavy advertising and it worked. However, underneath it all, were many

incidents of price gouging, excessive fees and extreme interest rate hikes once

the American consumer was through their doors.

For example, people who took

adjustable loans years ago, were hit with terrible news over the last year and a

half that their payments would significantly

increase

and there wasn't anything they could do about it. The government

sat back and let them do it. People who were paying $500 per month for a

mortgage for 10, 15, years, were told out of nowhere the steady rate they had

for all that time was gone, and their payment doubled. This was the story of

many people, a large number of them losing their homes.

There were other cases of consumers

being defrauded out of their homes via Washington Mutual refusing payment or

allowing people to commit fraud in wiping out checking accounts homeowners used

to pay their bills. This was done to a retired U.S. colonel, among others, to

gain his valuable home with vast acreage. Killinger knew, and despite public

protest, stole the man's home and land. This is the kind of heartless animal he

is with no respect for the law.

Kerry Killinger

There have been complaints of

Washington Mutual holding checks longer than previously disclosed before

clearing them and using technicalities such as an item payable on an account

being put through at 1PM, while the funds that were previously deposited via

check not being available until 2PM, thus creating an overdraft of $27. Those

$27 dollar fees ad up and create a lot of revenue.

Many people complained of

Washington Mutual's poor account security practices in allowing individuals from

all over the world, unauthorized access to customers' checking accounts,

illegally deducting funds in internet and telephone scams. Many complaints

cropped up

online

of customers losing several thousand dollars a piece in this

manner, then being charged excessive, multiple overdraft fees, with Washington

Mutual refusing to cover the damage for the miscellaneous, fraudulent charges

they allowed.

Just this month, on March 6, 2008,

there was a story in the Miami Herald about Washington Mutual ATM machines

spitting out receipts for transactions BUT NO CASH.

Other banks followed many of these

corrupt practices pioneered by Washington Mutual and Countrywide, to boost

revenue, and today we are witnessing the collapse of the U.S. banking industry

that created such a ripple effect that it severely harmed the insurance,

construction and furniture industries.